Spare Yourself the Quantum Hype. Book the Real Thing Early: Inside Creotech’s Hidden Gem.

Don’t Bet on Quantum Miracles. Bet on the Picks and Shovels Being Sold.

Introduction

In recent days, it is becoming more and more clear that the AI bubble is about to burst. I don’t know the future, but tech valuations are painfully high (which is why I shifted some investments toward other sectors, as disclosed here, and why I now focus only on truly superior tech companies — and only at a fair price — as explained here).

Regardless of what happens when the AI bubble deflates, you can be sure about one thing: despite all the tech talk about singularity and transhumanism, human nature does not change. And what does that mean for us? You can expect new bubbles to come!

In some circles, people already claim that quantum computing will be the next big bubble. I wouldn’t state that with certainty—especially since a smaller wave of hype has already come and gone—but it’s true that enthusiasm around quantum technologies has been building for years and keeps resurfacing. The “advent of quantum computing” has been announced multiple times, often with confident statements that we’re just “five years away”. Those promises have been around for at least a decade, and yet scalable, fault-tolerant quantum computers remain a distant prospect.

While quantum computers remain many years — if not decades — away, one part of the quantum ecosystem is already in the commercial phase: Quantum Key Distribution (QKD). Unlike speculative quantum computing roadmaps, QKD is an established, deployable technology used today in secure communication networks, government infrastructures, and critical industries. Telecom operators are rolling out quantum-secured links, the EU is building its own EuroQCI network, and some companies already sell turnkey QKD systems. In other words, this is not theory — it’s an operational, revenue-generating segment of the quantum landscape. And this is precisely where our focus turns next.

Enter Creotech Quantum.

I promised (see the Manifest) that sometimes we’ll look into non-obvious places — including spin-offs and businesses buried inside larger entities.

So here is one: not purely cybersecurity, but close enough to deserve attention.

Why “hidden”? Because you still can’t buy this company directly, even though it already exists as an independent entity. It has been carved out from its parent but is not yet publicly traded, so the only way to gain exposure is indirectly through the parent company.

The company in question is Creotech Quantum — a business that has already been formally separated from Creotech Instruments S.A. (CRI) and is now preparing for its public-market debut.

Before we dive into the quantum part, it’s worth starting with the parent company. For now, if someone wants exposure to Creotech Quantum, it can only be achieved by holding CRI shares.

Creotech Instruments — the Parent Company

Creotech Instruments is a Poland-based deep-tech company specialising in advanced space technologies, high-reliability electronics, and specialised hardware, including components used in quantum systems.

The company is the designer and creator of the proprietary HyperSat multi-purpose microsatellite platform intended for space missions. Its core activities include the design, production, and sale of advanced subsystems and systems used across several high-technology domains.

Operationally, the business is structured into four segments:

1. Space – designing, manufacturing, and selling subsystems and systems used in the space industry, including satellite components and complete microsatellite solutions based on the HyperSat platform.

2. Geospatial – developing systems for drone-operation management and for the generation, processing, and distribution of satellite and UAV data.

3. Quantum Systems [now → Creotech Quantum S.A.] – designing and producing subsystems and systems used in quantum computers, quantum cryptography (including QKD), time-synchronization systems, and other scientific or research applications.

4. Manufacturing – providing contract manufacturing services for industrial-grade electronics tailored to customer specifications.

Across these areas, the company supplies hardware and high-reliability electronics to space agencies, scientific institutions, commercial operators, and enterprises requiring advanced satellite, quantum, or geospatial solutions.

Customers worth particular mention?

European Space Agency (ESA) — Creotech delivers subsystems and has secured contracts with ESA.

European Organization for Nuclear Research (CERN) — Creotech has supplied advanced electronics/control hardware for scientific research.

Creotech Instruments - General Info (*)

🏢 Company name: Creotech Instruments S.A.

🏛️ Stock exchange: Warsaw Stock Exchange

🆔 ISIN: PLCRTCH00017

🔖 Ticker: CRI.WA

📈 Stock price: PLN 359 (≈ $97 at time of writing)

💰 Market cap: ~PLN 1024M (≈ $276M)

*Note: This applies to Creotech Instruments, the parent company. Our focus will be on Creotech Quantum, the soon-to-be in market spin-off.

Here’s a chart of Creotech Instruments (a parent company) for last year (courtesy of Yahoo Finance).

1. Business Description

When it comes to Creotech Instruments, the parent company, here comes just a short recap:

Poland’s leading space & deep-tech hardware company

Known for satellite subsystems, high-reliability electronics, FPGA-based systems

Long-term ESA/CERN collaborations

Reputation for engineering quality and government-grade projects

Now let’s move to its Quantum Systems division — recently carved out as Creotech Quantum S.A.

Established in June 2025, the new company builds its business on four core pillars:

1. Secure Communication (QKD)

Quantum Key Distribution systems based on fundamental laws of quantum physics, enabling communication security that cannot be broken by quantum computers or any current or future classical computing methods.

2. Quantum-Processor Control & Error Correction (Sinara)

Control systems for commercially built quantum computers, based on the Sinara family of electronics, along with the development of cryogenic integrated circuits for managing ion-trap processors (a project under the EU’s Quantum Flagship programme).

3. Precision Time Synchronisation (White Rabbit)

Hardware solutions enabling distribution of an atomic-clock-grade time and frequency reference within critical infrastructure, while simultaneously transmitting classical data over the same medium.

4. Astronomical Cameras

Development of the advanced CreoSky 6000 SST astronomical camera, designed for ground-based observational applications, including observatories and QKD ground stations.

It is the QKD systems segment that is especially interesting. Why did it catch our attention? Because it sits directly at the intersection of quantum technologies and cybersecurity — which makes it very much “our” domain here at CyberMoat.

A look into CIA & QKD

When discussing the pillars of cybersecurity, we often talk about CIA triad, which is one of the core foundational models in information security. It defines the three fundamental goals of cybersecurity: Confidentiality (ensuring that information is accessible only to authorized parties), Integrity (ensuring that information is accurate, unaltered, and trustworthy) and Availability (ensuring systems and data are accessible when needed).

One of the key mechanisms used to achieve Confidentiality—and indirectly support Integrity—is encryption, which protects data by transforming it using cryptographic keys.

Traditionally, organizations rely on symmetric encryption (fast and efficient, but requiring both parties to somehow share the same secret key) or asymmetric encryption (stronger for secure key exchange but significantly slower and more computationally expensive). This creates a fundamental tension: symmetric cryptography is highly performant but suffers from the classic key distribution problem, while asymmetric cryptography solves key exchange but introduces overhead and scalability issues. (And, let’s add, while asymmetric cryptography offers very strong protection against traditional computers today, it is expected to be easily broken by sufficiently powerful quantum computers in the future).

This challenge around how to securely establish encryption keys in the first place is exactly where Quantum Key Distribution (QKD) enters the picture—providing a radically different, physics-based method of exchanging keys with provable security guarantees and no reliance on computational hardness assumptions.

So what exactly is Quantum Key Distribution (QKD)?

QKD is a quantum-physics-based method for securely exchanging encryption keys.

It relies on the behavior of photons (for example, their polarization) and on a fundamental rule of quantum mechanics: measuring a quantum state inevitably disturbs it.

This leads to a powerful security property:

If an attacker tries to eavesdrop on the quantum channel

The quantum states of the photons change

And the communicating parties can immediately detect the intrusion

This gives QKD a unique advantage: you can detect interception.

QKD is designed not for everyday consumer use, but to protect extremely sensitive and mission-critical systems—the kind operated by governments, intelligence agencies, military infrastructure, and national financial backbones. In an era of rising geopolitical tensions, states are increasingly wary of relying on foreign cryptographic hardware or software that could contain hidden vulnerabilities, backdoors, or simply be weakened by future quantum breakthroughs. QKD offers an alternative: a security mechanism rooted not in mathematical assumptions or vendor trust, but in the fundamental laws of physics. For countries seeking technological sovereignty and long-term strategic assurance, this creates a niche where QKD becomes not just useful, but strategically irresistible. Needless to say, this creates a wide moat for companies such as Creotech Quantum.

Creotech Quantum leads eCAUSIS, an EU-funded programme developing a fully European QKD system — including the devices, key components, network-integration software, and a complete key-management system (KMS). In 2025 the company continued work on its second, smaller QKD module and presented the system publicly during QCI Days in Athens. The commercial launch is planned for 2026, making it one of the very few Europe-made QKD products. Creotech Quantum owns 100% of the IP, giving it full control over further development and commercialisation.

The company is also delivering three QKD-related projects for the European Space Agency (ESA), focused on ground-station components and measurement systems. This builds its capability to integrate QKD infrastructure for both public institutions and high-security commercial clients, such as critical-infrastructure operators, banks, and energy networks.

While QKD systems are likely to be the most important part of Creotech Quantum’s offering, the company is active in several other layers of the quantum-technology stack. These are not quantum computers themselves — which, for now, exist mostly as experimental prototypes with far too few stable qubits to be economically useful — but rather the infrastructure and components that the quantum ecosystem depends on. And it may well turn out that, especially if a “quantum bubble” inflates in the coming years, the best businesses will resemble the gold-rush era: the companies selling shovels, not necessarily the ones digging for gold.

Quantum Control Systems

Creotech Quantum develops high-precision control and measurement electronics intended for quantum-technology research and development laboratories. These systems operate at the “control layer” of the quantum stack: generating low-noise signals, synchronising measurements, and interfacing with the hardware environment that underpins qubit platforms.

This is a real market today — every quantum-research lab, corporate R&D project, or early-stage quantum-processor initiative requires such systems long before a commercially meaningful quantum computer exists. Creotech competes here with established players like Zurich Instruments and Quantum Machines, but offers a fully European alternative with its own engineering strengths.

White Rabbit Time-Synchronisation Systems

Another product line entering the quantum spin-off is based on White Rabbit, a time-synchronisation technology originally developed at CERN. White Rabbit enables sub-nanosecond accuracy across distributed systems over standard fibre networks.

This capability is valuable in telecom, finance, scientific facilities, and industrial automation — anywhere precise timing is essential. Creotech recently joined the global White Rabbit Collaboration, positioning the company within the standard-setting and development process of this highly specialised infrastructure technology.

Scientific Cameras and Advanced Electronics

Creotech Quantum will also offer high-sensitivity, high-speed scientific cameras and specialised electronics used in research, metrology, and industrial environments. While narrower in scope, this segment leverages the company’s long-standing expertise in high-reliability electronics developed for space and scientific applications. It also provides a steady, non-speculative revenue component within the broader deep-tech portfolio.

2. Quality Of The Management

Creotech Quantum will be led by Dr Anna Kamińska, one of the most experienced quantum-technology leaders in Poland and a long-standing pillar of its parent company, Creotech Instruments. With over eight years driving the company’s quantum initiatives, she has built and scaled Creotech’s Quantum Systems division from scratch, co-creating products now used in top global labs developing ion-trap and cold-atom quantum computers. Her scientific background includes a PhD in physics from the University of Warsaw and research experience at CERN, Oxford, DESY and JGU Mainz. She also serves as an expert to the European Commission, co-authored key EU quantum-strategy documents, and is active in European and NATO quantum-industry networks.

In short: Creotech Quantum starts with strong, internationally seasoned leadership.

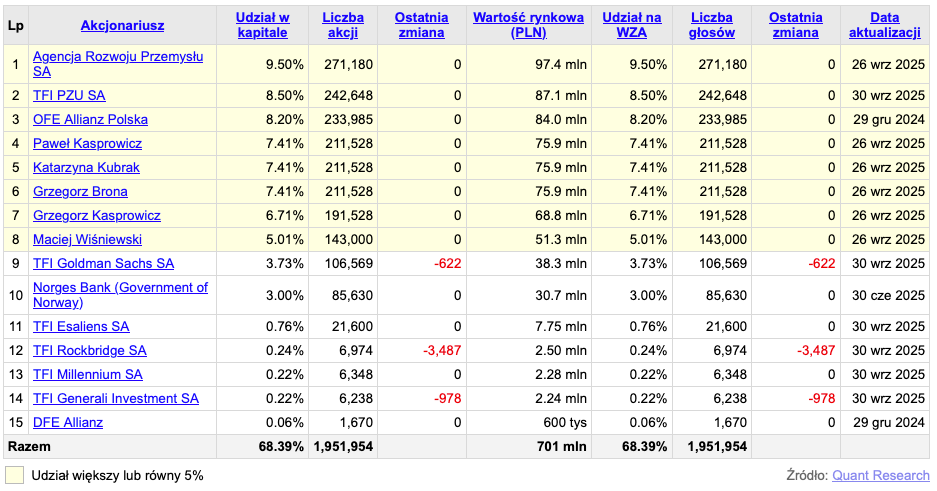

3. Shareholder Structure

According to the company’s announcement, when the quantum division is spun off into Creotech Quantum, existing shareholders of Creotech Instruments will receive shares in the new entity on a pro rata basis.

Hence, it is reasonable to assume for now that the shareholder base of Creotech Quantum will mirror that of Creotech Instruments (i.e., same proportional ownership, via a 1:1 split of rights).

However, this remains subject to corporate approvals, regulator (Komisja Nadzoru Finansowego) review of a prospectus, and the actual listing of the spin-off.

The shareholder base of Creotech Instruments — and likely Creotech Quantum after the 1:1 spin-off — is exceptionally stable and long-term oriented. The largest investor is the state-owned Agencja Rozwoju Przemysłu (9.5%), followed by major domestic institutions such as TFI PZU (8.5%) and OFE Allianz (8.2%). Several key early backers also remain heavily invested, including Paweł Kasprowicz, Katarzyna Kubrak and Grzegorz Brona (CEO), each holding 7.4%, as well as Grzegorz Kasprowicz (6.7%) and Maciej Wiśniewski (5.0%). In total, the top shareholders collectively control almost two-thirds of the company, giving Creotech a rare combination of ownership continuity, strategic commitment and strong alignment — a structure that should naturally carry over to the newly formed Creotech Quantum.

4. A Moat

The next question is whether the company has a sustainable competitive advantage — in other words, a moat.

In short: yes.

Quantum technologies are not something that can be built overnight or prototyped in a garage. They require deep physics expertise, years of laboratory experience, advanced electronics, stable infrastructure, and access to the global research ecosystem. This creates a natural moat: only a handful of players worldwide are truly capable of developing mature quantum-communication or quantum-computing technologies — and even fewer exist within the European Union. With Europe aggressively pushing for technological sovereignty in quantum communication, the company is positioned directly at the intersection of a fast-growing market and a strategically protected technology stack.

Creotech Quantum enters this space not as a startup, but with nearly a decade of accumulated know-how, proven products used in top global labs, and a 50-person engineering team. The barriers to entry are enormous, and the competitive field is exceptionally narrow — which is precisely why this spin-off is so strategically important.

5. End Market Attractiveness

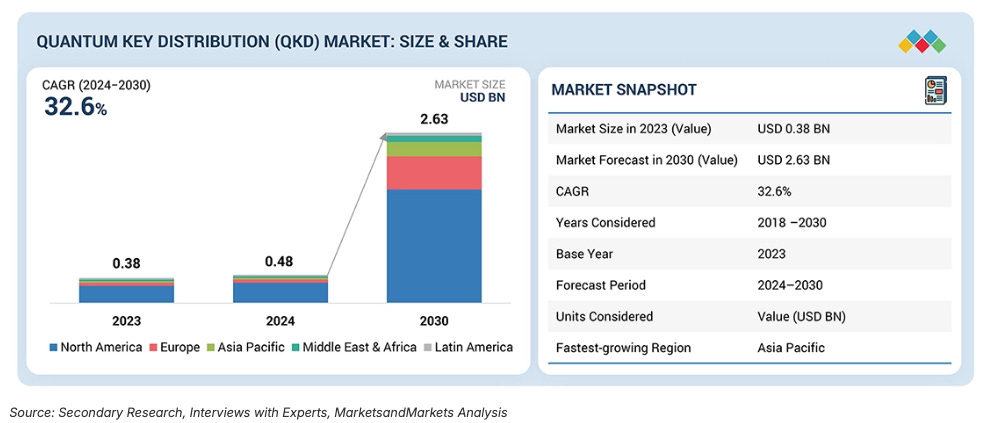

According to MarketsandMarkets, the Quantum Key Distribution (QKD) market is expected to grow at an enormous CAGR of ~32.6% (take it with a grain of salt, though) between 2024 and 2030, rising from USD 0.48 billion to USD 2.63 billion. This is one of the fastest-growing security-technology segments globally — and Europe is projected to be the fastest-expanding region.

Interestingly, the MarketsandMarkets research does not include Creotech Quantum at all (the report was published before the spin-off was announced). This further supports the view that the Quantum segment remains largely hidden — overshadowed by Creotech Instruments’ primary activity in the space sector.

Coming back to Quantum Key Distribution — it is worth pointing out that QKD addresses a strategic, long-term problem: the coming era of “harvest now, decrypt later,” where sensitive data intercepted today may be broken by quantum computers tomorrow. Demand is driven by governments, defence, finance, telecoms, and operators of critical infrastructure — precisely the domains where long-horizon security matters most.

The competitive landscape in quantum communication — especially in Quantum Key Distribution (QKD) — is remarkably thin. As Anna Kamińska notes in an interview, there are only two truly mature players worldwide with commercially proven QKD products: ID Quantique (IDQ) from Switzerland (recently acquired by IonQ for an estimated hundreds of millions of dollars) and Toshiba, which also develops advanced QKD systems. Beyond these two, the market consists mainly of small university spin-offs and early-stage startups, particularly in Europe. In other words: there are very few capable competitors globally, and even fewer within the European Union, which is precisely why EU governments and institutions are pushing for local, sovereign solutions. This scarcity of mature providers — coupled with high technological barriers — creates a rare strategic opportunity for Creotech Quantum.

6. Financials (early-stage limitations)

Ordinarily, this part of the analysis would dive into the usual fundamentals:

balance sheet strength,

capital intensity and future funding needs,

historical profitability and return on capital,

management’s capital allocation track record,

past growth rates,

and the overall financial resilience of the business.

But in this case, we simply can’t do that yet.

Creotech Quantum is not a stand-alone company today — it is a business segment being carved out of Creotech Instruments, and will only become a separate public entity after the spin-off. Financial statements for the new company do not yet exist, and its standalone cost base, margins, or capital structure are not formally defined.

It also isn’t profitable yet, which is normal at this stage of the quantum-technology lifecycle. Early scaling in deep-tech is capital-intensive and front-loaded.

However, one point is worth highlighting.

As Anna Kamińska emphasized in the interview, the quantum division already generates 8–10 million PLN in annual revenue. This is important for two reasons:

This is not an idea-stage startup.

The company already sells real, globally deployed products used in quantum labs and pilot infrastructures.

There is visible commercial traction.

Years of R&D have already converted into paying customers — something extremely rare among early European quantum-tech firms.

So while we cannot yet apply the full financial toolkit, we can say this:

Creotech Quantum starts its life with existing revenue, existing customers, and mature products — not with PowerPoint slides.

For a deep-tech spin-off, that is a meaningful starting advantage.

7. Valuation (attempted)

Valuation: What Can We Say at This Stage?

Before we even begin, one thing must be clear: we simply do not have enough financial parameters to perform a standard valuation analysis.

Creotech Quantum does not yet exist as a standalone listed company. We do not have:

separate cost structure,

standalone margins,

CAPEX requirements,

historical profitability,

or capital-allocation track record.

So what can we reasonably use?

Given the early stage and the available data, the only meaningful metric we can apply for comparison — however limited — is Price-to-Sales (P/S).

It’s not perfect, but in this specific context, it’s perhaps the best we have.

A Note on Peer Comparison: IonQ as the Only Real Option

Another challenge in valuing Creotech Quantum is that there are almost no publicly traded companies operating in the same niche. Quantum Key Distribution (QKD), quantum-control electronics, and quantum-communication infrastructure are still at the very beginning of commercialisation. Most players are either:

private (ID Quantique until recently),

tiny university spin-offs,

or divisions inside much larger conglomerates (e.g., Toshiba), where quantum accounts for a fraction of a percent of revenue.

This means that for now there is only one meaningful listed peer we can use as a reference point: IonQ.

IonQ is not a perfect comparator — it focuses on quantum computing, cloud access, and long-term research bets. But after acquiring ID Quantique, the global leader in commercial QKD systems, it now has direct exposure to the same strategic layer of the quantum stack that Creotech Quantum is targeting: quantum-secure communication and critical-infrastructure protection.

Other public quantum companies (like Rigetti, D-Wave, QUBT) operate in different technological domains and have no mature QKD or quantum-communication offerings. They do not serve as appropriate valuation benchmarks. Toshiba, on the other hand, is indeed active in QKD — but as a multi-billion-dollar conglomerate, it is not a usable pure-play comparison, as quantum segment is just a small fraction of their revenues.

As a result, IonQ becomes the “least bad” — and in practical terms, the only — public proxy for investor sentiment and valuation multiples in this sector.

This is why our relative valuation must rely on Price-to-Sales (P/S) versus IonQ. It’s imperfect for sure, but within today’s quantum-technology landscape, it’s the only realistic yardstick available.

Imperfect Comparison: IonQ

Having the above mentioned limitations in mind, we can still look at IonQ and compare Creotech Quantum metrics against it, since, after all:

both operate in the core quantum-technology stack, supplying critical infrastructure for quantum systems.

IonQ recently acquired ID Quantique, the world’s leading QKD (Quantum Key Distribution) company — which directly overlaps with Creotech Quantum’s ambitions in quantum communication.

Both companies are part of the deep-tech quantum ecosystem, not classical IT, cybersecurity, or semiconductor companies.

So from a sector perspective, they share enough DNA to justify using IonQ as a high-level valuation anchor.

So, let’s look at our most exciting part — the numbers!

The Internal Valuation Anchor: 72.99 PLN per Share

In the official division plan (Plan Podziału, source), Creotech assigns:

72.99 PLN per Creotech Quantum share

At a PLN→USD factor of ~0.27 → ~19.70 USD per share

Total number of CQ shares: 2,854,347

Implied equity value: 208.3 million PLN → ~56 million USD

So unless the market disagrees, Creotech Quantum begins life at an implied valuation of ~56 million USD.

For a company already generating 8–10 million PLN in annual revenue (~2.2–2.7 million USD), this translates to:

📌 Implied P/S ≈ 20–25×

This is high in absolute terms — but very modest for the quantum-tech sector.

It is worth noting that the 8–10 million PLN annual revenue estimate is rather conservative. The most recent report report shows that in just the first half of 2025, the Quantum Segment of Creotech Instruments generated over 8 million PLN on its own.

How Does This Compare to a Global Peer, IonQ?

Current third-party data shows IonQ trading at an astonishing:

~155× P/S — GuruFocus (gurufocus.com)

~148× P/S — StockAnalysis (stockanalysis.com)

~153× P/S — YCharts (ycharts.com)

And this all now, when there a major correction is on the way!

In other words:

📌 IonQ trades at ~140–160× P/S.

📌 Creotech Quantum’s implied entry P/S is ~20–25×.

This is 6–7× lower than the quantum-tech benchmark.

Moreover, IonQ’s historical valuation underscores just how extreme investor sentiment can be in the quantum-technology sector. Over the past years, IonQ’s Price-to-Sales (P/S) ratio has ranged from a low of 46.12 to a high of 1,539.2, with a historical mean of 223.46 (source). These numbers illustrate a simple but important point: when the market believes in the long-term potential of quantum technology, valuations can disconnect dramatically from present revenues (or — disconnect from reality). Against that backdrop, the implied P/S of ~20–25× for Creotech Quantum (based on its internal 72.99 PLN/share valuation) appears modest indeed.

Is this a perfect comparison? Absolutely not.

Different scale, different markets, different customers — and IonQ prices in massive future growth.

But given that we currently lack better parameters (EBITDA, FCF, profitability, ROIC, etc.), P/S is the only common yardstick we can use — and under that lens, the spin-off appears:

➡️ conservatively valued,

➡️ early-stage,

➡️ but not overhyped relative to global peers.

What This Doesn’t Mean

This is not a claim that CQ “should” trade at 150× sales (it is a crazy valuation, for any company, if you ask me).

Creotech Quantum valuation will depend on:

roadmap execution,

contracts won,

government adoption of QKD,

scaling of the product line,

and competitive dynamics.

But it does mean:

Creotech Quantum is entering the market at a valuation far lower than global quantum players — and with real products and revenue already in hand.

8. Risks

Like any investment, Creotech Quantum comes with its own set of risks. The most significant ones include:

1. Customer Concentration

Creotech’s client base consists primarily of large institutional customers — ESA, CERN, research centres, and government-linked entities. These contracts are high-quality but limited in number, meaning revenue can be lumpy and dependent on winning a few large tenders rather than broad, repeatable commercial sales.

2. Long Sales Cycles

Space, quantum, and scientific infrastructure markets operate on multi-year procurement timelines. Even when the technology is strong, revenues do not scale quickly. This makes planning difficult and limits short-term visibility.

3. High R&D Intensity and Capital Needs

Quantum systems, satellite subsystems, and precision electronics all require continuous R&D investment. Grants help, but eventually equity raises and dilution become likely — especially for the quantum spin-off, which will need funding long before it becomes profitable.

4. Early-Stage Quantum Market Uncertainty

While QKD and control electronics are already in commercial use, the broader quantum computing industry remains experimental. Demand is real but small, fragmented, and rather highly dependent on government or research budgets. Growth projections are easy to overstate.

5. Competition from Global Players

The company competes with well-capitalized international players (e.g., Keysight, Zurich Instruments, Thales Alenia Space). Some markets, particularly quantum control and space electronics, have global leaders with deeper pockets and wider distribution.

6. Execution Risk in the Spin-off

Separating Creotech Quantum into an independent company introduces operational and managerial challenges. The new entity must build its own processes, secure financing, and operate without the full organizational backing of the parent.

7. Regulatory and Geopolitical Exposure

Space and quantum technologies intersect with defense, dual-use regulations, and international export controls. Regulatory changes or geopolitical tensions may affect supply chains, project timelines, and access to components.

8. Limited Financial History

As the quantum business is pre-profit and does not yet have standalone financials, investors lack data on margins, cost structure, capital efficiency, or long-term unit economics. This increases uncertainty and complicates valuation.

9. Future

Creotech Quantum S.A. is now moving into the final stage of becoming an independent, publicly traded company. In September 2025, the company submitted its prospectus to the Komisja Nadzoru Finansowego (KNF) — the Polish Financial Supervision Authority, responsible for approving prospectuses and overseeing public markets. This filing is a key regulatory step toward listing the company on the main market of the Warsaw Stock Exchange.

The quantum division was formally carved out into a separate entity in June 2025, and the planned listing of Creotech Quantum is expected by the second quarter of 2026. The spin-off follows a classic structure:

shareholders of Creotech Instruments will automatically receive shares in Creotech Quantum, proportional to their holdings in the parent company.

In other words, if one wants exposure to Creotech Quantum before the IPO, the only path is through owning CRI shares today.

On the operational side, the company’s roadmap is quite clear. Creotech Quantum is preparing the commercial launch of its QKD system in 2026 — a product already undergoing prototype testing within the EuroQCI network. Additional early revenue streams are expected from ultra-precise time-synchronisation systems (White Rabbit) and quantum-control electronics, with broader ambitions over the next four years as quantum-communication markets mature and satellite-based QKD enters deployment.

Creotech Quantum is positioning itself as one of the few European companies operating across multiple practical layers of the quantum-technology stack — and the spin-off will finally bring this hidden segment of Creotech Instruments into the open market.

Summary

We’re not here to chase hype or jump onto the “quantum is the next big thing” storyline — because the future is too uncertain. Our focus is on what already exists today: technologies that are commercialised, deployed, and generating real revenue.

We’re not interested in fashionable, zero-revenue quantum startups that may never deliver anything tangible. Instead, we’re looking at a capable, engineering-driven deep-tech company with actual products, established revenue streams, and meaningful long-term potential.

We’re also not dealing with the usual extreme price-to-sales multiples that dominate the global quantum-technology space. Here, we’re looking at a company trading at a measured, conservative P/S ratio — especially rare in this sector.

To sum up, we’re not speculating on distant dreams; we’re analysing a company with real technology, real revenue, and real prospects — hidden inside its parent until the upcoming spin-off finally brings it into the open.

That’s it for now, stay tuned!

Michał

Disclaimer

This is not investment advice. I’m not professionally qualified — just sharing my personal analysis.