Z władzą ludową nie będziesz się nudził — Markets Rotate, Narratives Shift

On gold volatility, Bitcoin supply mechanics, SaaS repricing, and the shifting center of capital.

Introduction

“Z władzą ludową nie będziesz się nudził” — roughly translated, “With the People’s Government, boredom was never the problem.” was a sarcastic saying commonly heard in communist-era Poland (1945–1989), when the country operated under a centrally planned system officially branded as “people’s rule.” In practice, it meant constant economic distortions, unpredictable regulations, shortages, policy experiments, propaganda campaigns, and periodic “reforms” that rarely solved the underlying structural problems. Stability was scarce, surprises were not.

We find it a surprisingly fitting analogy for the multitude of recent economic and political events unfolding across the world. From an economic perspective, the current global financial architecture — built on fractional-reserve banking and Keynesian orthodoxy — is at least as structurally absurd as the centrally planned systems it once claimed moral superiority over (or perhaps, on second thought, even more so — a subject we will, God willing, explore at a less hectic time).

From a political perspective, we have few illusions. What appears to be emerging is not classical totalitarianism in its crude, brutal form, but something more technocratic — smoother in language, more data-driven, yet similar in nature.

The parallels are not difficult to spot. One of them is the permanent absence of boredom. The emerging “World People’s Government”, together with its tech brothers (yes — communists were always fond of brotherhood, remember), is doing its best to ensure we remain constantly occupied.

This dynamic, of course, applies to financial markets as well — constantly generating new “opportunities.” Since we are currently rather busy, we will limit ourselves to a brief update on a few selected topics.

Gold Rush?

Recently, markets were shaken by sharp price swings in gold and silver, with silver posting particularly violent reversals.

At CyberMoat, we are not metal fanatics. In fact, we are somewhat skeptical about long-term investments in metals (a mildly surprising position for someone with Austrian leanings, perhaps).

Not because we despise gold — but for several structural reasons. Before listing them explicitly, let us share two broader observations.

First, metals — like most commodities and natural resources — tend, over the very long term, to become cheaper in real terms. The popular narrative of permanent scarcity is largely a myth. On a planetary scale, we have barely scratched the surface. What changes is not physical availability but the cost of extraction. Mining may become temporarily more expensive as we move to lower-grade deposits, but technological progress repeatedly offsets these pressures through efficiency gains. History shows this pattern again and again. There can certainly be short-term shortages — frost destroying coffee crops, geopolitical disruptions, energy bottlenecks — but these are cyclical distortions, not secular inevitabilities.

Second, gold does occupy a special category. Annual supply growth is low (typically around 1–2%), and production cannot be ramped up easily. There are solid reasons why gold served as money for thousands of years — and continues to serve as a reserve asset even for central banks that publicly discourage private ownership while quietly accumulating it themselves. In that sense, gold is structurally superior to most other commodities, including silver.

However, even gold has limitations as an investment asset.

It produces no cash flow. No dividends, no internal compounding mechanism.

Its “growth” is largely a function of fiat currency debasement. Measured in weakening paper currencies, gold appears to rise. However, that process is neither linear nor mechanically tied to official inflation prints. Central banks and large financial institutions can influence liquidity conditions, and the fractional-reserve nature of the banking system inherently produces economic cycles — credit expansions followed by contractions — which distort the debasement process. Gold does not move in a simple 1:1 relationship with money supply growth or CPI. It experiences prolonged periods of stagnation, sharp repricing phases, and sometimes multi-decade flat real returns. A glance at a 50-year chart makes this painfully clear:

XAUUSD, 50Y, linear scale, source: http://stooq.pl Gold peaked at approximately $850 per ounce in January 1980. An investor who bought at that level would have remained under water for nearly three decades in nominal terms — gold did not sustainably exceed that price again until 2008.

Adjusted for inflation, the picture is even more sobering. According to U.S. CPI data (via in2013dollars.com), $850 in 1980 is equivalent to roughly $2,000 in 2005 dollars and over $3,200–$3,400 in today’s dollars, depending on the exact month used. Gold only convincingly surpassed that inflation-adjusted 1980 peak in 2023–2024 (two years ago!).

In practical terms, an unfortunate buyer at the January 1980 high has only just — more than four decades later — recovered his original purchasing power.

Scarcity alone does not guarantee smooth compounding.

Implementation risk exists. Physical gold involves storage, security, and transaction friction. Paper gold introduces counterparty and structure risk — ETFs, certificates, and derivative exposure may not always represent fully allocated, redeemable metal. The probability of failure may be low, but it is not zero. Physical ownership removes digital blocking risk and traceability, but introduces theft and custody risks. There is no perfect solution.

Finally, there is policy risk. Gold markets have historically been subject to intervention. Central banks control a substantial portion of global reserves. While large-scale price suppression would also harm their own balance sheets and is therefore unlikely under normal conditions, in extreme systemic scenarios one cannot entirely exclude aggressive measures — including forced sales or coordinated pressure.

Silver deserves a separate remark. Unlike gold, which sits heavily on central bank balance sheets, silver trades predominantly through leveraged futures markets. The structure is concentrated, and history shows that large institutions are not immune to misconduct (to put it mildly).

In 2020, JPMorgan agreed to pay $920 million in penalties to resolve charges of manipulating precious metals futures through spoofing practices — one of the largest such settlements in financial history (U.S. Department of Justice, Sept 29, 2020). The case demonstrated that even in supposedly deep and liquid markets, price formation can be distorted by dominant participants.

This does not prove systematic long-term suppression, but it does confirm that concentrated positioning, leverage, and aggressive order-book tactics can produce abrupt and violent price moves. In such environments, smaller investors often absorb the damage when cascades unfold.

If you are wondering about the events in the end of January ’26, we will merely recall the line often attributed to Mark Twain: history does not repeat itself — but it often rhymes.

None of this means we do not intend to benefit from the current cycle.

We do — but indirectly.

Rather than holding metal itself, we are selectively positioned in gold- and silver-related companies. We keep the specific tickers private, as these positions are relatively illiquid and time-sensitive; public discussion would add little value. This is cyclical, tactical exposure — a side operation alongside our core, quality-driven investment process.

BTC

When discussing crypto assets, one must first distinguish Bitcoin from the multitude of other coins. As Saifedean Ammous argues in his excellent book The Bitcoin Standard (Chapter 10, “Altcoins”), most alternative tokens resemble discretionary central banking — flexible supply, changing rules, governance committees, and monetary policy subject to human intervention.

Bitcoin, in contrast, operates without a central authority and follows a predefined monetary schedule embedded in its protocol.

From a purely economic perspective, Bitcoin’s supply dynamics are straightforward. The current annual supply growth is roughly 0.85% — already lower than gold — and it will not remain even that high for long. The next halving will reduce new issuance by 50%, and the process repeats approximately every four years until the terminal supply of 21 million coins is reached around the year 2140. With nearly 20 million already mined, more than 95% of total supply is effectively in circulation, while the remaining issuance declines asymptotically.

On paper, this creates a simple thesis: a strictly limited and increasingly scarce asset should appreciate over time if demand remains constant or grows.

But markets are not driven by arithmetic alone. They are driven by liquidity cycles, leverage, emotion — fear, greed, misunderstanding — and sometimes plain excess. Bitcoin is no exception.

The recent correction illustrates this dynamic. Despite alarming headlines, the move has been relatively contained by Bitcoin’s historical standards. From its peak above $120,000 to recent levels near $60,000, the drawdown is roughly 50%. Substantial, certainly — but far from unprecedented in Bitcoin’s history. More importantly, volatility appears structurally lower than in its early phases, when 70–80% drawdowns were not uncommon. Even traditionally “stable” assets can experience sharp dislocations: silver just recently had recorded single-session declines of over 30%, and companies widely regarded as ultra-conservative — such as Berkshire Hathaway — have endured drawdowns of roughly 50% on multiple occasions.

This suggests that, at least in terms of market structure, Bitcoin may be maturing.

That said, risks remain. Policy risk is obvious: governments retain regulatory leverage. Technological risk, while distant, cannot be dismissed entirely — advances in quantum computing, if ever capable of breaking current cryptographic standards, would pose a systemic threat (though mitigation pathways exist).

There is also the reputational overhang stemming from Bitcoin’s early days — anonymous origins, dark-web associations, and recurring conspiracy narratives. At various points, speculation — unsupported and widely debunked — has even attempted to link its creation to figures such as Jeffrey Epstein. Such episodes reinforce our point from yet different perspective: in a world where narratives spread faster than facts, “boredom” is rarely the problem.

SaaSPocalypse

SaaSPocalypse — a now infamous term first used on Wall Street by traders at Jefferies — described the violent sell-off in Software-as-a-Service stocks earlier this year. It wasn’t hyperbole: in a matter of days, hundreds of billions in market value evaporated as markets abruptly re-evaluated the durability of traditional software models.

The catalyst — at least in headline terms — was a seemingly innocuous set of AI tooling announcements from Anthropic. A new suite of tools designed to automate coding, research, and other workflows triggered sharp declines in shares of established software firms such as SAP, Salesforce, ServiceNow, and Workday.

What appeared to be just another product release crystallized a broader anxiety: that advanced AI could enable enterprises to build more software internally, drastically reduce the cost of custom development, and ultimately compress future demand for SaaS subscriptions.

Whether that fear is fully justified or partly reflexive is almost secondary. The market behaved as if it were real — and that reaction is the story.

Many of yesterday’s disruptors suddenly found themselves on the receiving end of disruption — not because capital mechanically migrated elsewhere overnight, but because expectations shifted. The acceleration of frontier AI — from OpenAI to ventures associated with Elon Musk — altered how investors perceived long-term defensibility across the software stack. Narrative gravity moved. Valuation multiples adjusted first. Business realities, as always, will adjust more slowly.

As we said before — z władzą ludową nie będziesz się nudził.

The markets were shaken once again. Power in capital markets is never static; it rotates. And when it rotates, valuations tend to adjust far faster than underlying business models.

As you may expect, at CyberMoat we do not subscribe to the simplistic thesis that “AI will disrupt everything.” It will disrupt many things — as technological step changes always do. Some companies will benefit, others will struggle. That is normal.

But the narrative that better code automatically destroys existing software businesses deserves scrutiny. Structural moats are not erased by a single release cycle. And valuation compression is not the same as business model extinction.

We do not have space here for a deep dive, so just a brief observation: it is not the code that makes a SaaS company great. Code, in itself, is not a durable competitive advantage. Any reasonably skilled team can write software. Yet not every software firm becomes Microsoft or Google.

Remember our Coca-Cola example when discussing Adobe? Any company in the world can produce a carbonated, sweetened beverage. The formula is not the moat — despite the mythology of the “secret recipe,” which is useful precisely because it distracts from the real source of advantage. Coca-Cola’s strength lies elsewhere: distribution, propaganda, brand, logistics, contracts, shelf space, and habit.

Software is similar: the real moat is not the code. The moat is integration into workflows, embeddedness in enterprise processes, customer support and service, regulatory compliance, contractual reliability, and accountability. It is one thing to generate a clever demo, but it is another to deploy a mission-critical system inside a regulated bank, ensure uptime, pass audits, integrate with legacy infrastructure, and stand behind it legally and operationally.

Do not assume that powerful, well-managed software companies will collapse simply because a teenager can “vibe-code” a prototype. If that were sufficient, markets would have been conquered long ago. What a teenager can build, thousands of others can build too. The real advantage lies elsewhere.

In short: code is not the edge. Distribution, trust, and security are.

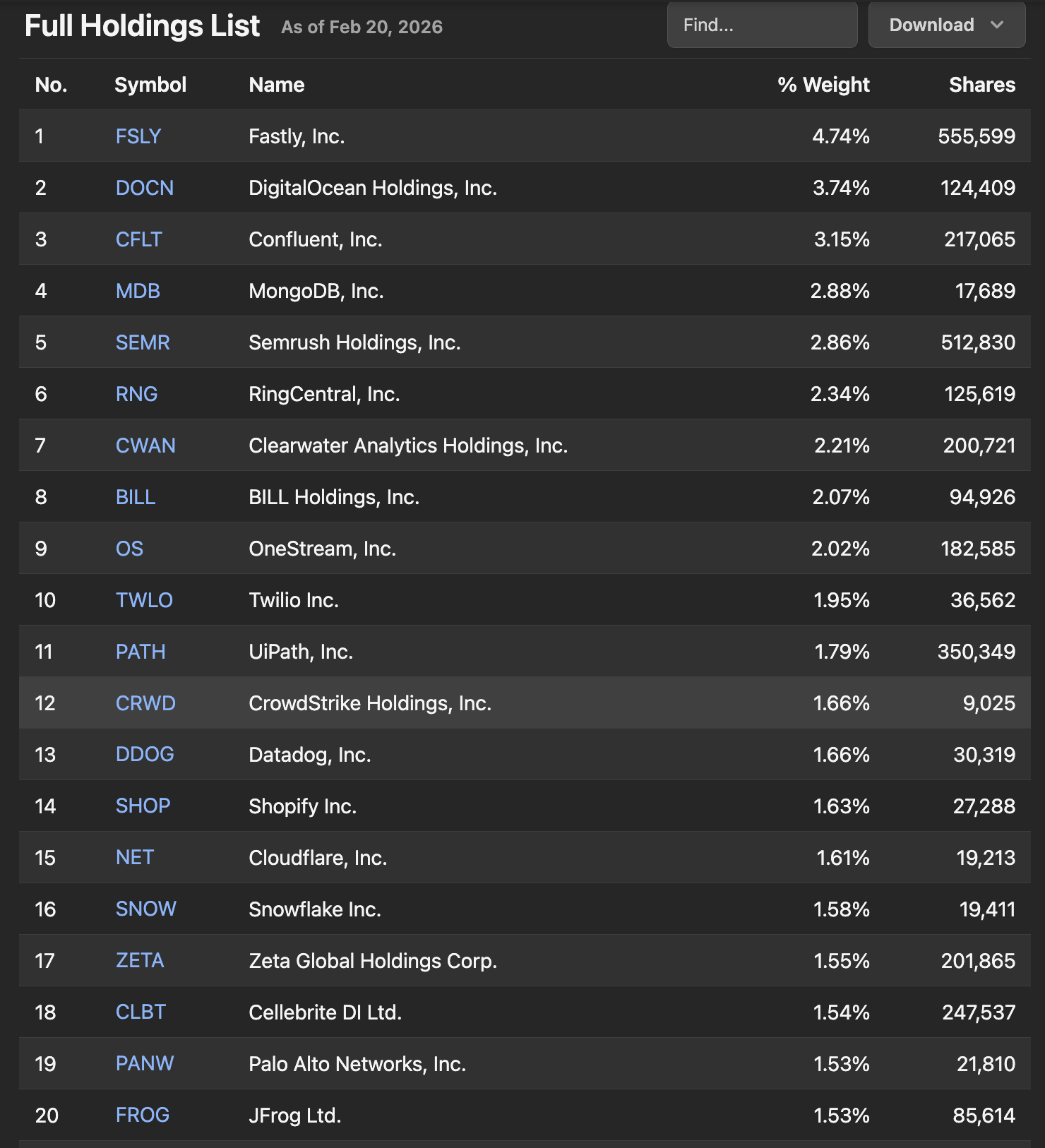

For a high-level view of the drawdown, one reasonable proxy is the WisdomTree Cloud Computing Fund (WCLD), an ETF tracking a basket of cloud-focused software companies. Its main holdings are Fastly, DigitalOcean, Confluent, MongoDB and several others, top 20 listed below:

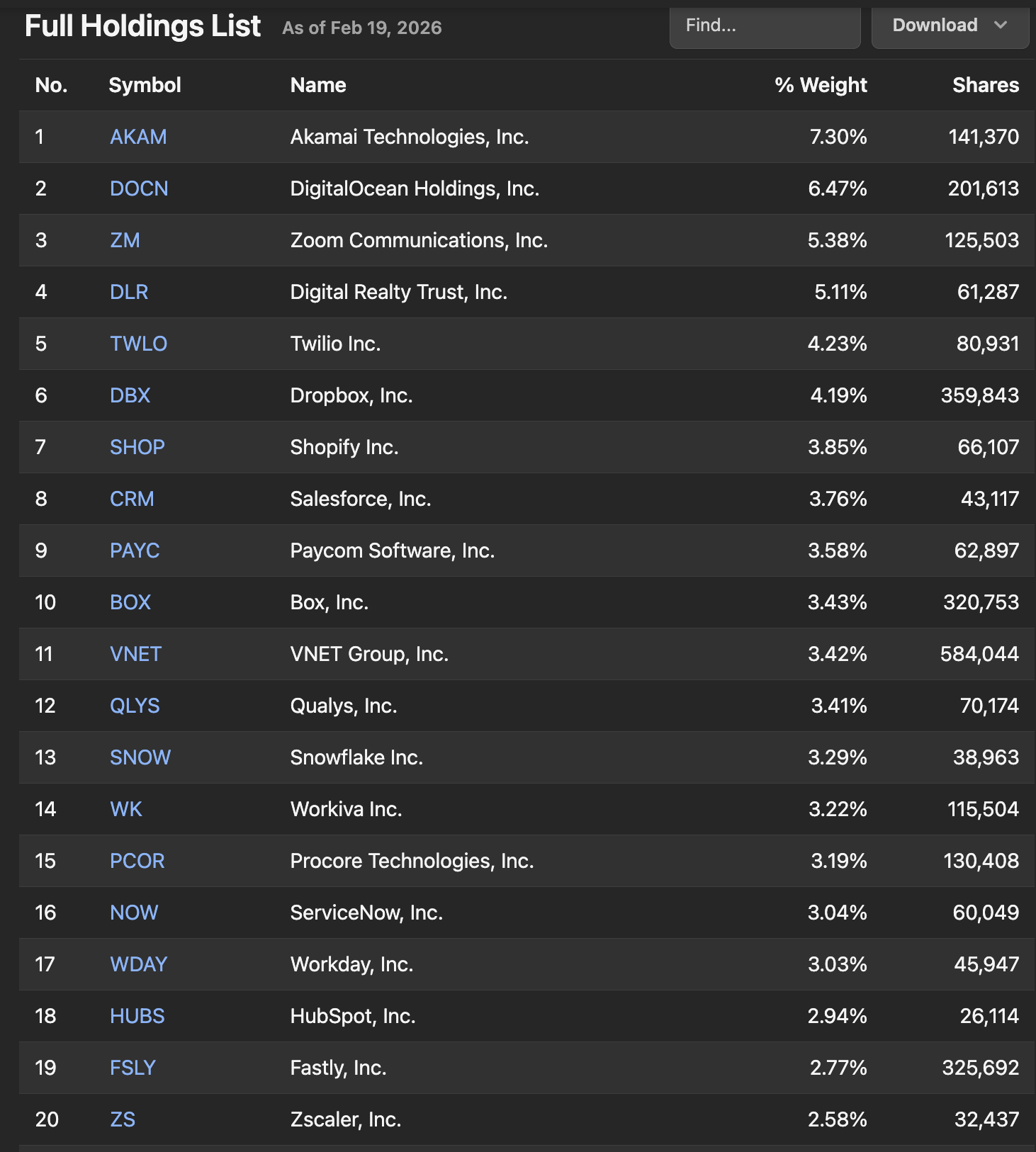

Another good proxy is Global X Cloud Computing ETF (CLOU) which tracks the ISE Cloud Computing Index, covering a broader set of cloud infrastructure and software players:

Large drawdowns often create opportunity for value investors. As Baron Rothschild allegedly said: “Buy when there’s blood in the streets, even if the blood is your own.”

But a word of caution is necessary. What may initially look like a bargain simply because the price has fallen sharply may not be a true bargain at all. Valuations in 2021–2022 were, in many cases, detached from economic reality. Similar, to smaller degree however, can be said about early 2025. A 50% or even 60% correction from an absurd price may merely return a stock to something resembling fair value — not deep value. In other words, one might be paying a normal price rather than securing a genuine margin of safety.

That said, we do believe real opportunities exist. In some cases, the sell-off appears excessive rather than merely corrective. Examples include Duolingo and Coursera, both of which we have recently added to our portfolio. We hope to share more detailed insights soon. Caveat emptor, however — do not replicate this move blindly unless you understand the risks and the underlying business models.

On a related note, the recent drawdown has — fortunately — also affected parts of the cybersecurity sector. As you may recall, we previously refrained from building positions in many cybersecurity names, as they were, in our assessment, either overpriced or, at best, fairly priced. That did not meet our investment risk criteria. This may have looked somewhat inconsistent — after all, CyberMoat focuses on investing and cybersecurity — but buying at inflated valuations is as much a mistake as ignoring opportunity elsewhere when prices are depressed.

Our objective is not to promote cybersecurity stocks at any cost. Our objective is to allocate capital prudently, generate returns, and sleep well at night.

There are several long-observed cybersecurity names now approaching levels that could justify entry. We are watching closely. Perhaps, finally, we may be able to step in — if price allows.

Data & Research Stack Update

Starting with this article, we are formally integrating StockAnalysis.com into the CyberMoat research workflow.

We have been using it privately for some time. This is not a trial run — it’s the result of deliberate testing.

What we were looking for was simple:

One place for financial statements

One place for ratios and valuation metrics

One place for screening

One place for portfolio tracking

Clean interface

Fast performance

No unnecessary noise

In short: a focused, professional-grade research environment without platform bloat.

StockAnalysis delivers institutional-quality financial data while remaining lightweight and fast. It avoids the visual clutter and upsell-heavy design common across many financial portals. From a workflow perspective, it is one of the most efficient environments we’ve used.

The key differentiator, however, is pricing.

At standard pricing ($79/year), it is already materially cheaper than many alternatives offering comparable data depth. With the current 20% annual promotion:

$63.20 for the first year

Then $79 per year thereafter

Monthly option: $9.99

At that level, the price-to-utility ratio becomes unusually attractive.

Historically, they rarely run discounts outside of Black Friday, so this is not a routine promotion.

For a serious investor who values speed, clean data access, and cost efficiency, this is a rational tool choice.

👉 https://stockanalysis.com/pro/?ref=cybermoat

Disclosure: CyberMoat participates in the Stock Analysis affiliate program. If you subscribe via our link, it supports the project at no additional cost to you.

Track Record – Cryptographic Commitments

Polish small caps – Positions opened Jan–Feb 2026

To ensure transparency while protecting liquidity and avoiding signaling risk, the following SHA-256 hashes represent timestamped commitments of two Polish small-cap positions initiated during Jan–Feb 2026.

These hashes encode the original disclosure strings (company identifier + purchase window + internal reference).

7a6fce2cabc9ad434be2b0f99f7301a42d6201f441367f7ea99bd0f6a622d623

1a3666cb348d9ed25f2c08e52e8f30caee7f30ba8a4464431b0a5aede346da92

- Michał, CyberMoat

Uncovering risks, securing opportunities.

Disclaimer

This material reflects personal views and is not investment advice. Positions may be held in securities discussed.